Understanding the New IRS Tax Code Changes for 2026: Key Deductions and Credits You Can’t Miss

The landscape of taxation is in a constant state of flux, and as we approach 2026, significant shifts in the IRS Tax Code 2026 are on the horizon. These changes are not merely minor adjustments; they represent a fundamental reshaping of how individuals and businesses will calculate their tax liabilities, affecting everything from everyday deductions to long-term financial planning. For anyone looking to optimize their financial health, staying informed about these impending modifications is not just beneficial, it’s absolutely crucial. This comprehensive guide aims to demystify the complex world of the IRS Tax Code 2026, providing a clear roadmap to understanding the key deductions and credits that will define the next era of tax compliance.

The year 2026 is particularly significant because it marks the sunset of several provisions introduced by the Tax Cuts and Jobs Act (TCJA) of 2017. This means that many of the tax breaks and adjustments that taxpayers have grown accustomed to will either revert to their pre-TCJA levels or be subject to new interpretations and regulations. The implications are far-reaching, impacting individual income tax rates, standard deductions, itemized deduction limitations, and various business tax incentives. Without a proactive approach to understanding these changes, taxpayers risk missing out on valuable opportunities for savings or, worse, facing unexpected tax burdens.

Our deep dive into the IRS Tax Code 2026 will cover a broad spectrum of topics, from the general overview of the expiring provisions to specific details on how these changes will affect your personal finances, investments, and business operations. We will explore the anticipated adjustments to individual income tax rates, the standard deduction, and personal exemptions, which are set to make a comeback. Furthermore, we will analyze the potential resurgence of limitations on itemized deductions, often referred to as the Pease limitation, and its impact on high-income earners. Beyond individual taxpayers, we will also touch upon the implications for businesses, particularly concerning the Section 199A qualified business income (QBI) deduction, which is also slated for expiration.

This article is designed to be your go-to resource for navigating the complexities of the IRS Tax Code 2026. We will break down intricate tax jargon into understandable language, offer practical advice, and highlight strategic planning opportunities to help you prepare effectively. Whether you are an individual taxpayer, a small business owner, or a financial professional, the insights provided here will equip you with the knowledge needed to make informed decisions and adapt to the evolving tax environment. By the end of this guide, you will have a comprehensive understanding of what to expect, how to prepare, and how to leverage the changes to your advantage, ensuring that you are well-positioned for financial success in 2026 and beyond.

The Sunset of TCJA Provisions: What to Expect from IRS Tax Code 2026

The Tax Cuts and Jobs Act (TCJA) of 2017 brought about the most significant overhaul of the U.S. tax system in decades. While many of its provisions were made permanent for corporations, a substantial number of individual tax provisions were set to expire at the end of 2025. This means that as of January 1, 2026, the IRS Tax Code 2026 will largely revert to pre-TCJA law unless Congress acts to extend, modify, or make permanent these expiring provisions. Understanding these sunset provisions is the first critical step in preparing for the changes ahead.

Individual Income Tax Rates Reversion

One of the most impactful changes will be the reversion of individual income tax rates. The TCJA reduced marginal tax rates across most income brackets. For instance, the top individual income tax rate was lowered from 39.6% to 37%. In 2026, these rates are scheduled to increase, with the top rate potentially returning to 39.6%. All other brackets will also see an upward adjustment. This means that many taxpayers could find themselves in a higher tax bracket, leading to a greater portion of their income being subject to taxation. Financial planning for the IRS Tax Code 2026 must consider these higher rates, especially for those in higher income tiers, to mitigate the impact on their take-home pay and overall financial strategy.

Changes to the Standard Deduction and Personal Exemptions

The TCJA significantly increased the standard deduction, nearly doubling it for all filing statuses, which simplified tax filing for many Americans. Concurrently, it eliminated personal exemptions. In 2026, the IRS Tax Code 2026 is set to bring back personal exemptions, while the standard deduction will revert to its pre-TCJA levels, adjusted for inflation. For many taxpayers, especially those who previously took the increased standard deduction, this shift could mean a higher taxable income. Families with multiple dependents, however, might find the reintroduction of personal exemptions beneficial, potentially offsetting some of the reduction in the standard deduction. It’s crucial to evaluate whether you will once again benefit from itemizing your deductions or if the new standard deduction, combined with personal exemptions, will still be the more advantageous option.

Reinstatement of Limitations on Itemized Deductions (Pease Limitation)

Another significant change impacting higher-income taxpayers is the potential reinstatement of the Pease limitation on itemized deductions. This provision, suspended by the TCJA, previously reduced the total amount of itemized deductions for high-income earners. Its return under the IRS Tax Code 2026 could substantially limit the tax benefits of deductions like state and local taxes (SALT), mortgage interest, and charitable contributions for wealthier individuals. Understanding this limitation is vital for strategic charitable giving and other itemized deduction planning. Taxpayers who previously relied heavily on these deductions will need to reassess their strategies to minimize their tax burden effectively.

Other Expiring Individual Provisions

Beyond these major changes, several other individual provisions from the TCJA are also scheduled to sunset. These include the elimination of miscellaneous itemized deductions subject to the 2% adjusted gross income (AGI) floor (e.g., unreimbursed employee expenses, tax preparation fees), the deduction for moving expenses (except for active-duty military), and the reduction in the mortgage interest deduction limit for new mortgages. The IRS Tax Code 2026 will see these provisions revert, potentially increasing the tax complexity and liability for certain groups of taxpayers. A thorough review of your current deductions and an understanding of how these expirations will affect you is paramount.

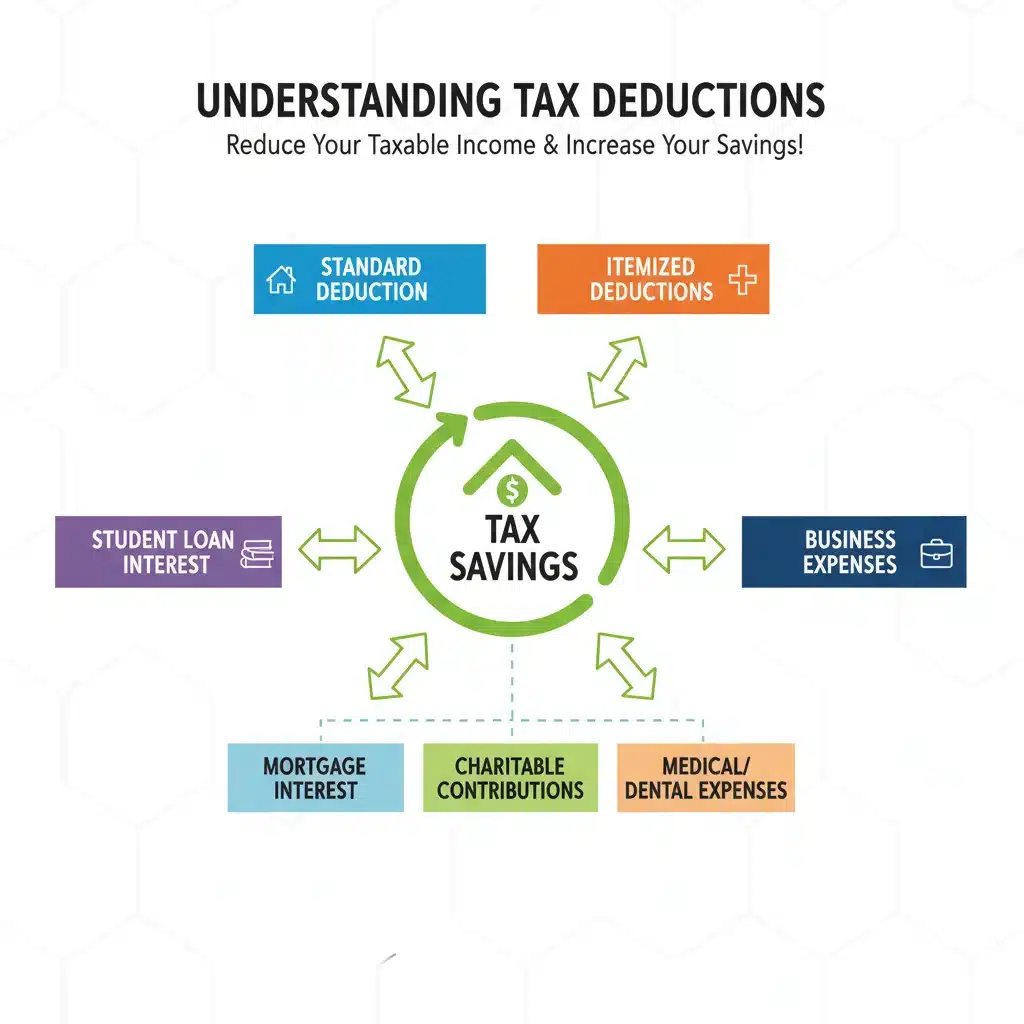

Key Deductions You Can’t Miss Under the IRS Tax Code 2026

While some deductions are set to expire or change significantly, many valuable deductions will remain, and some might even regain prominence under the IRS Tax Code 2026. Strategic utilization of these deductions is essential for minimizing your taxable income. Here, we delve into the key deductions that taxpayers should focus on as they prepare for the new tax landscape.

Mortgage Interest Deduction

The mortgage interest deduction has historically been a significant tax break for homeowners. While the TCJA reduced the limit for new mortgages to interest on up to $750,000 of qualified residence debt, this limit is set to revert to $1 million for mortgages taken out before December 15, 2017, and an increased limit for new mortgages under the IRS Tax Code 2026. For many homeowners, especially those with larger mortgages, understanding these limits and how they apply to their specific situation will be crucial. It’s important to differentiate between interest paid on acquisition debt (used to buy, build, or substantially improve a home) and home equity debt, as the deductibility rules can vary.

State and Local Tax (SALT) Deduction

The TCJA famously capped the SALT deduction at $10,000, a provision that disproportionately affected residents in high-tax states. While there is ongoing debate about an extension or modification of this cap, the default under the IRS Tax Code 2026 would be for the cap to revert to its pre-TCJA unlimited status. However, if the Pease limitation is reinstated, the benefit of an uncapped SALT deduction could be diminished for high-income earners. Taxpayers in states with high property and income taxes should closely monitor legislative developments regarding the SALT cap, as it could have a substantial impact on their tax liability.

Charitable Contributions

Charitable contributions remain a powerful way to reduce taxable income, and their rules are generally stable, though the AGI limits for cash contributions were temporarily increased during the pandemic. Under the IRS Tax Code 2026, taxpayers can typically deduct cash contributions up to 60% of their AGI and non-cash contributions up to 50% of their AGI, with carryover provisions for excess contributions. For those planning significant charitable giving, understanding the nuances of direct contributions, donor-advised funds, and qualified charitable distributions from IRAs can maximize tax efficiency. High-income earners should also be mindful of the potential reintroduction of the Pease limitation, which could indirectly affect the overall benefit of their charitable deductions.

Business Expense Deductions

For self-employed individuals and small business owners, various business expense deductions will continue to be vital. The IRS Tax Code 2026 will still allow deductions for ordinary and necessary business expenses, including home office deductions, business travel, vehicle expenses, and qualified retirement plan contributions. However, the Section 199A qualified business income (QBI) deduction, which allowed eligible pass-through entities to deduct up to 20% of their qualified business income, is set to expire. This expiration will significantly impact many small businesses and independent contractors, making it even more critical to maximize other available business deductions and explore alternative strategies for tax efficiency. Consulting with a tax professional to understand the implications of the QBI deduction’s expiration and to identify other viable deductions is highly recommended.

Education-Related Deductions

Education remains a key area for tax benefits. Deductions for student loan interest and tuition and fees (though the latter has seen frequent changes and extensions) are expected to persist under the IRS Tax Code 2026. The student loan interest deduction allows taxpayers to deduct up to $2,500 in student loan interest paid during the year, subject to income limitations. While the tuition and fees deduction can be more generous, its availability often depends on legislative extensions. Families planning for higher education or those currently repaying student loans should keep these deductions in mind. Furthermore, contributions to 529 plans, while not directly deductible at the federal level, offer tax-free growth and withdrawals for qualified education expenses, making them an excellent long-term savings vehicle.

Crucial Tax Credits You Can’t Miss Under the IRS Tax Code 2026

Tax credits are often more valuable than deductions because they directly reduce your tax liability dollar-for-dollar, rather than just reducing your taxable income. As the IRS Tax Code 2026 takes shape, understanding which credits are available and how to qualify for them will be paramount for maximizing your tax savings.

Child Tax Credit (CTC) and Credit for Other Dependents (ODC)

The TCJA significantly expanded the Child Tax Credit (CTC) to $2,000 per qualifying child, with up to $1,400 being refundable, and introduced the $500 Credit for Other Dependents (ODC). These enhancements are scheduled to revert to pre-TCJA levels in 2026, meaning the CTC could drop to $1,000 per child and the ODC might disappear. The IRS Tax Code 2026 will likely see a return to stricter income limitations and a lower overall credit amount. Families with children should prepare for a potentially reduced credit, which could impact their overall tax refunds or liabilities. Staying updated on any legislative efforts to extend or modify these credit amounts will be essential for family financial planning.

Earned Income Tax Credit (EITC)

The Earned Income Tax Credit (EITC) is a refundable tax credit for low-to moderate-income working individuals and families. This credit is not directly affected by the TCJA sunset provisions and will continue to be a vital support for many taxpayers under the IRS Tax Code 2026. The EITC amount varies significantly based on income, filing status, and the number of qualifying children. It’s crucial for eligible taxpayers to claim this credit, as it can result in a substantial refund. The IRS provides an EITC Assistant tool to help determine eligibility and estimate the credit amount.

Education Credits: American Opportunity Tax Credit (AOTC) and Lifetime Learning Credit (LLC)

Education credits remain a cornerstone of tax relief for students and their families. The American Opportunity Tax Credit (AOTC) offers up to $2,500 per eligible student for the first four years of higher education, with 40% of the credit being refundable. The Lifetime Learning Credit (LLC) provides up to $2,000 per tax return for undergraduate, graduate, or professional degree courses, or courses taken to acquire job skills. These credits are expected to remain available under the IRS Tax Code 2026, though income limitations apply. Families investing in education should carefully evaluate which credit they qualify for, as they cannot claim both for the same student in the same year.

Clean Energy and Energy Efficiency Credits

With a growing focus on environmental sustainability, various clean energy and energy efficiency credits have been introduced or expanded. These credits, often updated through legislation like the Inflation Reduction Act, encourage homeowners to invest in renewable energy sources (e.g., solar panels) and energy-efficient home improvements (e.g., specific windows, doors, insulation, and HVAC systems). The IRS Tax Code 2026 is expected to continue offering these incentives, providing valuable tax relief for those who make eco-friendly upgrades to their homes. Keeping abreast of the specific requirements and eligible improvements for these credits can lead to significant savings.

Retirement Savings Contributions Credit (Saver’s Credit)

The Retirement Savings Contributions Credit, also known as the Saver’s Credit, helps low- and moderate-income taxpayers save for retirement. This non-refundable credit can be up to $1,000 for individuals or $2,000 for married couples filing jointly, depending on their AGI and contributions to IRAs or employer-sponsored retirement plans. This credit is a powerful incentive for those who might otherwise struggle to save for retirement and is expected to continue under the IRS Tax Code 2026. It’s an often-overlooked credit that can significantly boost retirement savings efforts.

Strategic Planning for the IRS Tax Code 2026

Given the significant changes coming with the IRS Tax Code 2026, proactive and strategic planning is more important than ever. Waiting until tax season to understand these changes could lead to missed opportunities or unexpected tax liabilities. Here are key strategies to consider as you prepare for the new tax environment.

Review Your Withholding and Estimated Taxes

With potential changes to tax rates and the standard deduction, your current withholding or estimated tax payments might no longer be adequate. It’s crucial to review your W-4 form with your employer or adjust your estimated tax payments to avoid underpayment penalties. Use the IRS Tax Withholding Estimator to help you determine the correct amount. This proactive step ensures that you are paying the right amount of tax throughout the year, aligning with the impending IRS Tax Code 2026.

Reassess Your Itemization Strategy

As the standard deduction reverts to lower levels and personal exemptions return, many taxpayers who previously took the increased standard deduction might find it more advantageous to itemize their deductions once again. Gather documentation for potential itemized deductions such as medical expenses, state and local taxes (if the cap is lifted or you’re below it), mortgage interest, and charitable contributions. For high-income earners, understanding the potential impact of the Pease limitation on itemized deductions will be critical for effective planning under the IRS Tax Code 2026.

Optimize Retirement Contributions

Retirement accounts like 401(k)s and IRAs offer significant tax advantages, and maximizing contributions can help reduce your taxable income. Consider increasing your contributions to these accounts, especially if you anticipate being in a higher tax bracket in 2026. For those eligible, the Saver’s Credit can provide an additional incentive. Exploring advanced strategies like Roth conversions, particularly in years with lower income or before tax rates potentially increase, could also be beneficial under the evolving IRS Tax Code 2026.

Consider Tax-Loss Harvesting

For investors, tax-loss harvesting remains a valuable strategy. This involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income. With the potential for market fluctuations and the changing tax landscape, strategically realizing losses before 2026 could provide benefits. This strategy can be particularly effective if you anticipate higher capital gains tax rates in the future due to the IRS Tax Code 2026.

Consult a Tax Professional

The complexity of the impending changes makes consulting with a qualified tax professional or financial advisor invaluable. They can provide personalized advice based on your specific financial situation, helping you navigate the intricacies of the IRS Tax Code 2026. A professional can help you identify all applicable deductions and credits, formulate a comprehensive tax plan, and ensure you comply with all new regulations, ultimately optimizing your tax position and avoiding costly mistakes.

The Broader Economic Impact of IRS Tax Code 2026

The changes slated for the IRS Tax Code 2026 extend beyond individual and business balance sheets; they have the potential to ripple through the broader economy. Understanding these macroeconomic impacts can provide a more holistic view of the upcoming tax environment.

Impact on Consumer Spending and Investment

When individual income tax rates increase and certain deductions and credits diminish, households may experience a reduction in disposable income. This could lead to a decrease in consumer spending, which is a significant driver of economic growth. Conversely, the reintroduction of certain tax breaks or the adjustment of others could stimulate specific sectors of the economy. For instance, if clean energy credits remain robust, investments in renewable energy technologies and energy-efficient home improvements could see continued growth. The overall balance of these changes under the IRS Tax Code 2026 will dictate the net effect on consumer behavior and investment patterns.

Business Investment and Job Creation

For businesses, especially the expiration of the Section 199A QBI deduction, could influence investment decisions and job creation. While corporate tax rates set by the TCJA are permanent, changes affecting pass-through entities – which represent a vast majority of U.S. businesses – could impact their profitability and their capacity to expand. Businesses might re-evaluate their operational structures or investment strategies in response to the IRS Tax Code 2026. Policymakers will be closely watching these impacts to determine if further legislative action is needed to support economic stability and growth.

Potential for Legislative Action

It’s important to remember that the scheduled sunset of TCJA provisions is not set in stone. Congress always has the option to intervene, extend certain provisions, or introduce new legislation. The political climate and the economic conditions leading up to 2026 will undoubtedly play a significant role in shaping the final version of the IRS Tax Code 2026. Lobbying efforts from various interest groups, economic forecasts, and public opinion will all contribute to the ongoing debate. Staying informed about political developments and potential legislative proposals is therefore an integral part of preparing for these tax changes.

Conclusion: Preparing for Your Tax Future with IRS Tax Code 2026

The impending IRS Tax Code 2026 changes represent a critical juncture for taxpayers across the United States. From the reversion of individual income tax rates and the adjustments to the standard deduction and personal exemptions, to the potential reintroduction of itemized deduction limitations and the expiration of the Section 199A QBI deduction, the tax landscape is poised for a significant transformation. Ignoring these changes is not an option for anyone serious about sound financial management.

Proactive planning, informed decision-making, and, where necessary, expert guidance are the pillars upon which successful navigation of the IRS Tax Code 2026 will rest. By understanding the sunset provisions, identifying key deductions and credits that will remain or reappear, and implementing strategic financial adjustments, you can not only mitigate potential negative impacts but also uncover new opportunities for tax savings. Reviewing your withholding, reassessing your itemization strategy, optimizing retirement contributions, and considering tax-loss harvesting are all actionable steps you can take now.

Ultimately, the goal is to ensure that you are well-prepared for any shift the IRS Tax Code 2026 brings, positioning yourself for financial resilience and growth. Don’t wait until the last minute; start your preparation today. Engage with tax resources, consult with professionals, and stay informed about legislative developments. Your financial well-being in the coming years depends on it.